In 2018, New York Times writer Nellie Bowles told the story of a “crypto utopia” emerging on the island of Puerto Rico. There, entrepreneurs — mostly men who had struck gold by effectively gambling on the efficacy of cryptocurrencies (i.e., digital currency) — had left behind their California dreams in favor of “a new city where the money was virtual and the contracts are all public.” Their pursuit was, on its face, a humanist one: to demonstrate a world where power and wealth are decentralized. One could even, theoretically, call it socialist.

But in typical failed utopia fashion, their decentralized “crypto future,” where free-market principles reigned supreme, manifested itself not as a project chasing a new world order, but rather an incubator for a bunch of newly wealthy iconoclasts dodging taxes. There was, in other words, very little new about this “new world” other than the fact that the money had been turned into lines of code, and the roadmap was all too familiar: New technology had been exploited and propagandized as the next step in the quest for some ephemeral Eden. In reality, digital currency was just the latest technological mechanism serving a new generation of the same people.

By now, if you know anything about cryptocurrencies, chances are you’ve drawn your own conclusions, most of which are unlikely to summon hope for any sort of utopia. But the same can’t be said of blockchain — the technology that underpins digital currencies and acts as a sort of digital ledger. In the simplest terms, “a blockchain,” according to Block Geeks, is “a time-stamped series of immutable records of data that is managed by a cluster of computers not owned by any single entity.” That means the records are public and verifiable, and since there’s no central location, it’s much harder to hack, considering the digital ledger exists simultaneously in millions of places. Up to now, blockchain has gained its reputation as the technological backbone for an emerging decentralized monetary system — one that, while innovative, still falls prey to the ills of capitalism, generating wealth for the few at the expense of the many.

But what if blockchain, in its purest sense, wasn’t just another capitalist exploit? What if, for example, the highly transparent and decentralized nature of blockchain’s system for recording information in a way that makes it difficult or impossible to change, hack or cheat, could be leveraged as a way to provide housing as a human right?

That’s one proposal set forth by Adrian, the founder of the podcast Blockchain Socialist. “Let’s say we’re in Mushroom Kingdom,” he says, referring to a fictional setting from the Mario franchise. In this version, Mario is a single dad with a kid, and “Luigi is a single guy,” says Adrian. Under this socialized world, everyone gets access to housing, represented by a housing token on blockchain. “This token gives you access to a certain amount of square feet in a home,” he explains. “Mario’s token gives him access to a slightly bigger double apartment because he has a kid, so he’s entitled to more square feet of space because that agreement, which is democratically decided upon, is coded into blockchain.” In other words, a blockchain isn’t just an algorithm managing units of information, like a normal database, but rather it’s being used to encode and even define how that information is executed, with real-life implications.

Adrian was “working a really low paying job” when he first learned about cryptocurrencies. “I needed to figure out a way to also pay for my student loans and was learning more about stocks for investment, so I took a closer look at crypto,” he says. In the beginning, Adrian tells me that if he wanted to look up the most basic information about blockchain, “70 percent of it would be very right-wing and conservative” discourse about why Bitcoin has value. The emphasis, he says, was on the scarcity of Bitcoin and its similarities, in that way, to the gold standard. “Bitcoin never appealed to me, but Ethereum [another prominent digital currency] did because of smart contracts.”

Smart contracts were first proposed in the early 1990s by computer scientist and cryptographer Nick Szabo. Simply put, what distinguishes a smart contract from a regular digital contract is that it’s self-enforcing: It’s not the sort of computer program that makes a recommendation to a person about how they should control a digital asset, but rather a program that controls the digital asset itself, using the conditions of an agreement, with the terms of the agreement between buyer and seller directly written into lines of code. The code not only executes the contract, then, but means that the transactions are trackable and irreversible. The advantage here is that they allow transactions to be carried out without “the need for a central authority, legal system or external enforcement mechanism,” according to Investopedia. In that sense, they’re often compared to vending machines: You put money in, you get something in return. If you don’t put money in, you get nothing.

For Adrian, the concept of a decentralized network where lines of code execute decisions rather than a governing body was a clear fit with socialism. “I thought this could actually automate a lot of functions [performed by] people who work in finance, the state, etc., or automate the function of capitalists,” he says. The idea, he continues, closely aligns itself with a statement made by Friedrich Engels, the 19th century German socialist, about replacing “the government of persons by the administration of things.” And blockchain (or something like it), Adrian believes, is a possible answer to this. “You can automate these different technocratic areas of state and bureaucracy so you don’t have to worry about the technocratic elite.”

Though this may all sound futuristic, it’s not, particularly with regard to the realm of property ownership — in 2018, the first million-dollar house in the U.S. was sold on blockchain using digital currency. It’s not difficult to see why blockchain technology became a natural fit for the real estate industry, either, “Partially because real estate relies on databases of property and keeping track of who owns the property,” says Adrian.

But living under capitalism, Adrian points out, it’s easy to tell the direction this digitized technology database for the real estate industry is likely headed. One ultimate conclusion is smart locks. “In a dystopian capitalist blockchain world, you’ll likely see real estate being tracked on blockchain,” he says. If the tenant hasn’t paid their rent or mortgage payment for that month, the bank or landlord can use this technology to make sure the house is kept locked until payment is recorded on blockchain (the specious argument from libertarians is that using this blockchain technology to enact evictions is less violent than calling the cops).

Adrian, however, is suggesting an entirely different approach — a socialist use for this same technology, effectively swapping the lock for a key that grants a person’s right to a home. “I’m no techno-utopian,” he says. “There has to be social change that goes along with this process.” But, he says, “we cannot stop the progress of innovation in technology. We need, instead, to think of alternatives using that same technology.”

None of this will come easily, or intuitively for that matter. Ben Tarnoff, a tech worker, writer and co-founder of Logic Magazine, tells me that libertarian politics aren’t merely “the social milieu of blockchain; they are embedded into the technical organization of blockchain itself.” In other words, though blockchain is in fact decentralized, it’s a libertarian vehicle and its most basic aim is to take monetary sovereignty away from state institutions.

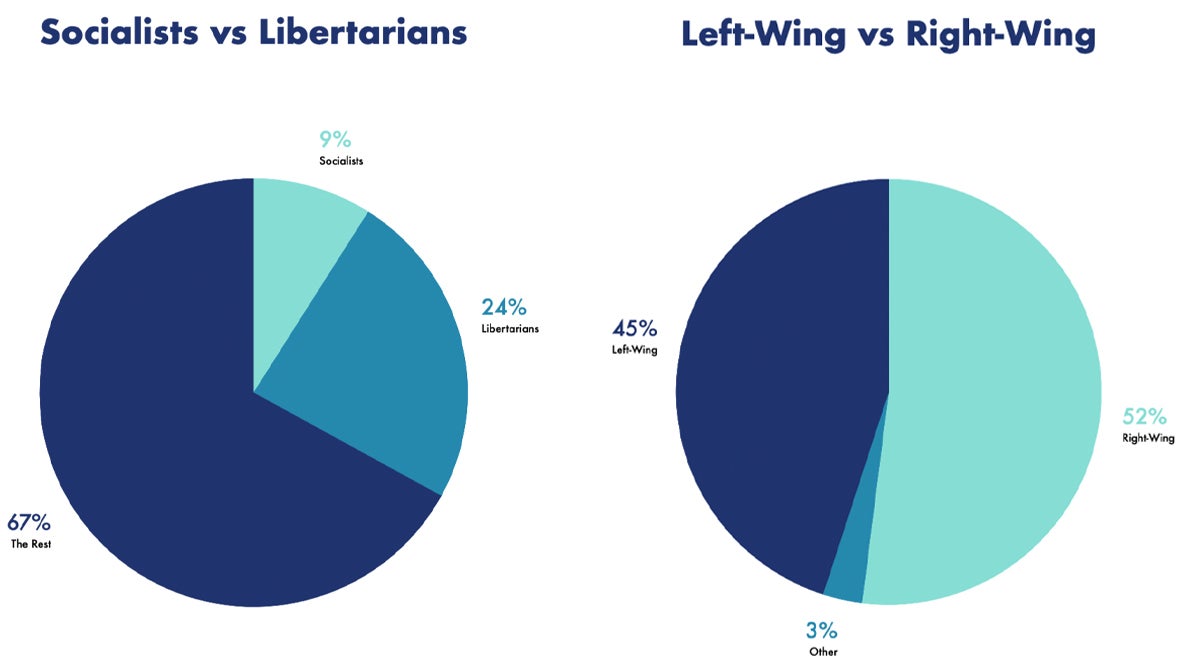

Two years ago, Coindesk, a prominent blockchain media outlet, surveyed their community and found that amongst the 1,200 respondents, socialists made up only nine percent of the cryptocurrency community, and libertarians accounted for 24 percent. “After combining categories into our composite of the left vs. right spectrum, we observe that 52 percent of the crypto community are right-wing and 45 percent identify as being on the left,” per their report.

The findings are difficult to accept for people like Adrian who are trying to apply the technology toward socialist ends. But they’re hardly surprising — after all, a decentralized system also means there’s little in the way of regulations, which places a lot of trust in the social fabric of the network. Paraphrasing political theorist Langdon Winner, Tarnoff says that blockchain socialists “may find their own politics colliding with the politics of the artifact.”

Mark Alizart, a philosopher and writer well known in the blockchain-socialist space, sees the “artifact” differently. “Blockchains, per se, are socialist, inasmuch as they’re social means of creating value,” he tells me. Another major innovation of blockchain technology that appeals to socialists is that it’s a digital ledger that relies on a community of validators to verify every new block that’s added to the database. In that sense, he explains that if Marxist theory proposes giving ownership of banks back to the people, cryptocurrencies could help take down the state. “Bitcoin and other blockchains sure have that goal in mind,” he says. “So I really think socialists should consider them as one of the most powerful levers to further their agenda.”

Not doing so, he says, could be a death knell for the left, especially since, up to this point, Alizart believes that technophobia has destroyed “the very soul of the left from within.” To survive, then, the “left has to embrace technology or perish.” “Because ultimately, technology is about a better world,” he says. “It’s about the end of alienation to work. It is about ending poverty and famine.” But he distinguishes that the implementation of technology has to be collectively appropriated, otherwise it can become a dangerous tool to implement “cyber feudalism.” “It can only be done if people get involved in it instead of turning their back and dreaming of returning to the 19th century,” Alizart adds.

The collective approach is what drew Aleeza Howitt — an independent researcher working in the area of alternative currencies and government-independent universal basic income projects — to blockchain. Howitt has also heard all the arguments against why cryptocurrencies can’t be leveraged for progressive political means. “They’re wasteful, as in energy inefficient [it takes 15,000-kilowatt-hours to produce $0.85 Bitcoin],” she says. Or they have a regressive monetary policy: “Bitcoin is kind of like digital gold.” Not to mention that within Bitcoin, wealth inequalities are staggering. “These arguments, they’re valid, but they’re not arguments against blockchain,” Howitt tells me. “They’re not arguments against technology. They’re arguments against the ways that people have used the technology.”

Howitt says they mainly stem from a misconception about the really innovative idea behind blockchain. “The conversation is usually dominated by people out there to make a quick buck,” she says. “That’s the kind of stuff that gets in the news — Bitcoin millionaires and stuff like that.” What you don’t see, she tells me, is the articles about all these “cool alternative governance systems that people are experimenting with.”

Through independent research on universal basic income, monetary reform and alternative currencies, Howitt paved her own idea of blockchain’s potential. “My interests were influenced by the Occupy Wall Street movement,” she says. “I went traveling for a bit, which gave me exposure to alternative exchange systems and a more global perspective. I think poverty is structural, and we need to end it.”

One project Howitt is currently working on, for which she’s actively looking for communities interested in local currencies to pilot the project, is a blockchain-based mutual credit platform called Trustlines Protocol. The app, which is currently in beta and running on the Trustlines Blockchain, is peer-to-peer mutual credit. On Trustlines, “friends can pay you for goods and services by issuing IOUs that will increase your balance, and reduce theirs.”

The philosophy of money creation in Trustlines Protocol is what sets it apart. The vast majority of money these days is so-called “bank money,” which is really debt issued by commercial banks. Applications like Venmo or Paypal are just a layer on top of that standard monetary system. “But Trustlines is a return to an organic, decentralized form of money that’s just credits issued between trusted people — we call it ‘people-powered money,’” says Howitt. That’s why, she adds, “you have so much freedom to experiment with using different units of value.” “It’s not just dollars or euros,” she explains. “It’s also, you can use time hours, kilowatt-hours — you could even use units of beer.”

Because the source code for these public blockchains exist on millions of computers throughout the world, they’re not only completely transparent and immutable but impossible to shut down, which in turn makes blockchain ideal for experimenting with different ways of governance or economic policy, according to Howitt.

Again, the idea here is to automate as much as possible to get reliable, incorruptible and accessible systems. “Using cryptocurrency, it’s kind of radically transparent,” says Howitt. “The funds that you use, it’s public information where your money is going.” Even though users can choose to stay pseudonymous, all transactions are public, unless you’re using tools specifically designed for privacy. For that reason, blockchain, according to Howitt, is ideal for managing public sums of money. Furthermore, she says that if you want to have your public funds connected to a democratic system where people vote virtually on who to allocate the funds to, you can.

Howitt uses the example of BrightID, a social identity network and another decentralized project for which she’s a contributor, as an example of how funds can be managed with transparency by a “decentralized autonomous organization” commonly referred to as a DAO. “For example, the BrightID Main DAO that holds funds is like a robot,” she says. Though its managers are real people, acting as a board of directors, the robot automatically does whatever they vote for it to do, and as a bonus, it’s totally transparent so anyone can audit the whole thing. “If the vote passes, the agreement goes through — like a vending machine,” she says.

As noted, though, despite Howitt’s “close-knit group of friends that are all involved in similarly progressive blockchain projects,” the cryptocurrency community is still largely dominated by libertarian ideology. The reddit community r/cryptoleftists, founded in 2018, still only has 1,300 members. “What I don’t like is that a lot of basic information is hidden behind technical jargon and also financial jargon,” Howitt says, as to one reason why these more altruistic blockchain projects have yet to take off. “A lot of the most innovative projects are obscured by questions about, what’s the token price?” This subsequently makes it unappealing to the left writ large. But Howitt insists that the important stuff isn’t how much the price of Ether [a digital currency] is right now — instead, she’s interested in what people are building on the platform, Ethereum.

In his book Red-Green Revolution: The Politics and Technology of Ecosocialism, professor Victor Wallis writes that “technology is not neutral,” and it never has been. The point of blockchain socialism or a socialist perspective of blockchain, then, is to present a choice that isn’t against technology, but one that is against the perversion of technology by capital. In a phone conversation, Wallis brings my attention to ancient technology used in agricultural development in the Andes where, at 12,000 feet, water is scarce, and the formation of vertical waterways via terraces allows rainwater to be distributed more equally. “It’s really fantastic what they’ve built there, and it works very well,” Wallis explains. “Of course, machinery, heavy machinery wouldn’t work there at all, but the point is that what they’ve built isn’t for the market, it’s for their subsistence. They’re not at the mercy of the market to get their basic necessities.”

To that end, for socialists — at least the ones interested in technological innovation — blockchain presents a unique opportunity to free civilization from the market.

A utopian endeavor, no doubt.

Andrew Fiouzi

Andrew Fiouzi is a staff writer at MEL.