Isn’t it nice when siblings share the same interests? Like the Koch Brothers, whose kindred business acumen, up until younger brother David’s death in 2019, helped them pilot Koch Industries to its place as the second-largest privately owned company in the U.S. — and whose allied spending habits over the years led to them donating an estimated $100 million to conservative and libertarian causes. Or like their British equivalents, the secretive octogenarian twins the Barclays, who similarly built businesses together, became brother billionaires — and then acquired a stately old newspaper that has since become the U.K.’s print version of Fox News.

They also jointly invested in buying one of Britain’s actual Channel Islands so they could build an actual castle on it and live there. “It’s a great example of what can be achieved in this country,” David Barclay is reported to have said in 2000, on the occasion of he and his brother receiving their dual knighthood from the Queen, “from whatever background or education or humble beginnings.”

Truly, fairy-tale stuff!

When siblings join financial forces, it seems they can indeed achieve big things — up to and including world domination. A millisecond’s consideration of the world the rest of us live in, though, tells us that these sorts of simpatico attitudes toward profit and loss are very much the anomaly within families. From the pop-culture cliché of the dissolute loser sibling (see: Fredo Corleone, Uncle Buck, Oscar Bluth, Princess Margaret); from the alarming frequency of former presidents with bankruptcy-prone brothers; from that wayward aunt or uncle in our own families whose name always exhorted a dejected sigh around the dinner table; and from every Monopoly board ever flipped in fraternal exasperation — it’s clear that sisters and brothers aren’t merely dealt better or worse hands when it comes to business sense; they’re often throwing their chips around in completely different card games.

There’s growing evidence from psychologists and behavioral scientists that many of our personality traits — including how risky or responsible we are with our savings, career planning and investments — are more predetermined by our genes than we realize. Yet somehow, when it comes to brothers and sisters who, as well as a proportion of their genes, might also share the same home, same upbringing and same socioeconomic background, and who, while growing up, were exposed to all the same examples of money management as modeled by their parents, it’s so often another story entirely. When it comes to money matters, even those from happy homes are regularly baffled, disappointed, made envious and occasionally leeched dry, thanks to their siblings’ wildly incongruous attitudes to money, their working lives and what they consider a “super-generous” birthday present.

One clue as to why this might be, oddly enough, comes from recent research that indicates the genetic motives for financial behavior might be much stronger than we ever knew. In the early 2010s, Stephan Siegel, professor of finance and business economics at the University of Washington, collaborating with Miami Herbert Business School’s Henrik Cronqvist, utilized Sweden’s monumental twins registry to produce the most comprehensive series of analyses yet into the genetic basis of financial decision-making. And one thing “that came out of our research that was most surprising to ourselves,” he says, “especially for one of our colleagues who has three kids, is that the parental component, the nurture component, that we can identify seems to be relatively small, once you control for the genetic part.”

“One has to be very careful in interpreting this fact,” he adds. “But an extreme interpretation would mean that parents don’t matter once they’ve handed down their genetic material.”

There are a few caveats to this insight, as Siegel acknowledges. First, he cautions that in the wider world, where a range of cultures, social norms and economic restrictions muddy the statistical patterns and individual outcomes, such a stark reading would be “definitely not quite correct.” Another is the context: “One thing that we’ve always said is that our results apply to Sweden around the year 2000, and they aren’t necessarily transferable to any other setting in terms of geographic or cultural sense, or time.” At that point, the Swedish tax authorities kept scarily fastidious records of all citizens’ trades and transactions, and this provided Siegel with a golden opportunity to cross-reference this with data from the twins registry to examine the fiscal attitudes and life courses plotted by 30,000 twins — the money they saved, the risks they took and the investment biases they showed.

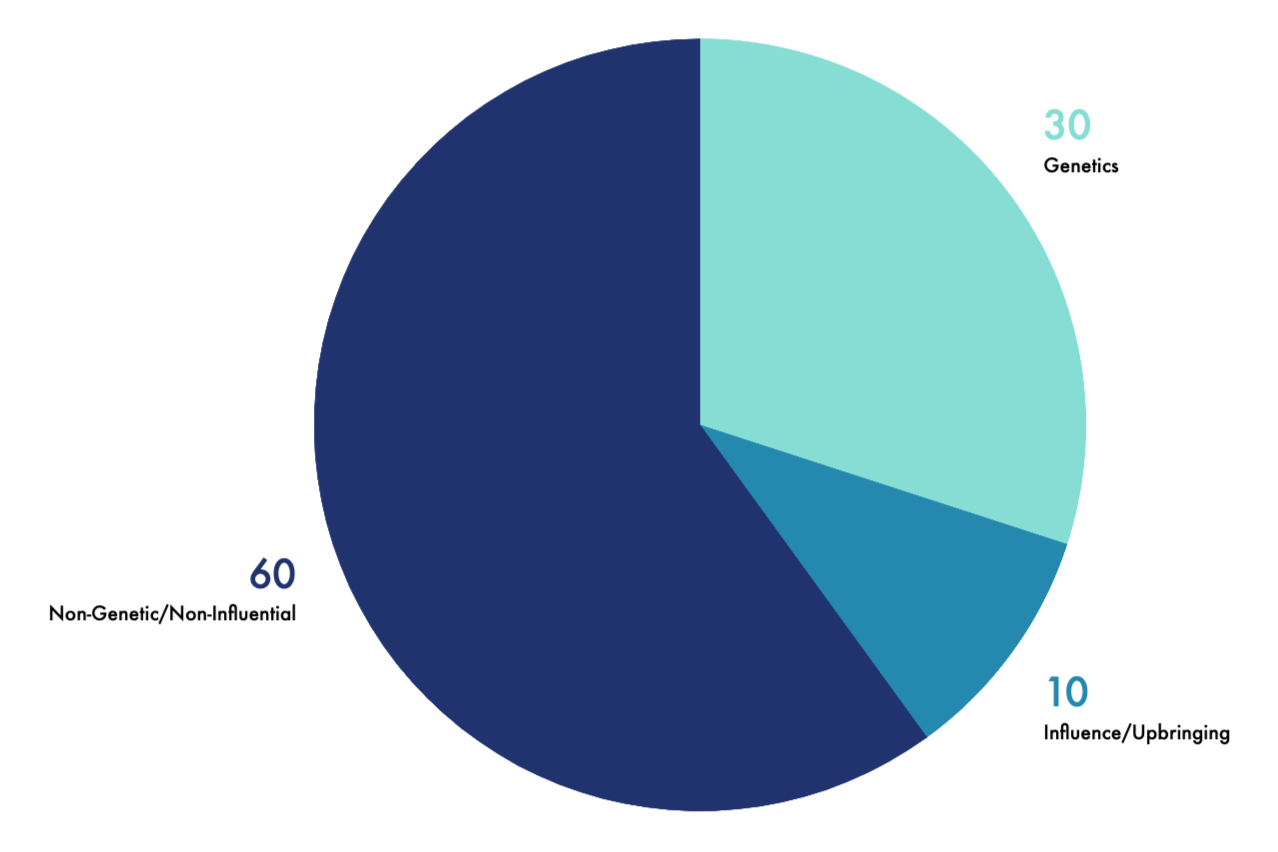

By comparing the set of identical twins (who share 100 percent of their genes) with the fraternal twins (who, like any pair of regular siblings, have just half of their genes in common), much of the complicating non-genetic influences that might sway their decision-making over time (such as their shared upbringings and socioeconomic background) could be neatly filtered out. Siegel’s analysis led him to the arresting conclusion that around one-third of the variability in people’s different financial outlooks and habits could be explained by the genes they inherited from their parents.

Putting to one side any idiosyncrasies around personal finance that might be specific to Swedish people, what this broadly suggests is that for all of us brought up in Western societies, our attitudes to money are far more embedded in our cells than most of us would assume. And it means that those money-related characteristics we tend to frame in terms of “frugality,” “irresponsibility,” “riskiness,” “career-mindedness,” “acquisitiveness,” “lack of ambition,” “success,” “a healthy disregard for the lifelong accumulation of wealth” — that sort of thing — are, as with our political views, driven much more by our DNA than we might like to think.

But how might all of this help explain why brothers and sisters so often exhibit conflicting philosophies when it comes to their bank accounts, retirement plans, commitment to jobs and the like? Surely a stronger steer from their genes would make close relatives more closely aligned on those sorts of things?

As Siegel points out, among the vast majority of sisters and brothers who are non-identical, the picture is always immediately complicated by the fact that they only share half their genes in common — and a different mix of psychological attributes from the same father and mother can easily result in strongly dissimilar personality traits.

He also argues that in societies where the right cultural conditions prevail — in which all children received a baseline in financial education, say, or where there was more of a level playing field in terms of economic opportunities — it’s likely that, on average, parents’ budgeting examples would matter even less to the development of their kids’ business brains. “That’s the general finding that other people have found,” says Siegel. “That the more nurturing there is, so the better the overall environment that people in general experience and grow up in, the stronger the genetic component actually becomes.”

This might seem counterintuitive, but at the aggregated level of population it makes sense, he suggests, “because it’s sort of saying that if you have a very supportive environment, then everyone is only limited by their genetic ability. If everything is ‘taken care of’ in terms of the environmental components, then how far you can go really depends more and more on what your body and your brain is capable of.”

Crucially, there is also the other two-thirds’ worth of influences to account for. “The twin model — comparing the identical with the fraternal twins — basically allows us to say: Out of 100 percent variation, how much is because of the genetic difference? And that’s about 30 percent. And then maybe another 10 percent is because of parents’ [influence via your upbringing] in our findings. And then the remaining 60 percent is everything else — that is, not genetic and not because of your parents.”

Eldest vs Boldest?

That “everything else” turns out to include a huge array of possible factors, many of them much harder to measure, with or without identical twins to help light the way. “My impression is that each of [these factors] account for a small fraction, but together they actually make up a huge chunk,” says Siegel. “It’s everything that makes you you; all the experiences that you had, and your sibling didn’t have, make up two-thirds or so of what you do and who you are.”

Though these more slippery substrata of financial character might be tougher to quantify, it’s not to say that psychologists — especially those interested in family dynamics and the repeated patterns in sibling relationships — haven’t invested a great deal of time in it. One of them, whose research has led her to similar conclusions to Siegel, though she’s approaching it from a very different direction, is Catherine Salmon, professor of psychology at the University of Redlands, and co-author of the book The Secret Power of Middle Children.

When it comes to financial deviation between siblings, Salmon breaks the set of influences into three broad areas: “For something like people’s approaches to things like finance and business strategies, a big chunk of that is going to be formed by the aspects of their personality that are influenced by genetics.” The second area is the “shared environment” — “which should be all the things that are the same in the family” — and she notes it’s become clear from research that (as Siegel’s findings also seem to indicate) this “doesn’t contribute much to many aspects of people’s personality and their approaches to things.”

For her, it’s the third set, the “non-shared environment,” equivalent to Siegel’s fragmented 60 percent contribution from external influences, that shapes siblings’ outlooks the most and accounts for much of the divergence in their career paths and spending patterns as their lives press on into adulthood. Elements in this non-shared environment would include major influences from outside the home, such as the distinct peer groups each brother or sister in a family end up affiliating with. But, she says, they “also include things like their birth order and sex differences and how they experience their family environment. I don’t know that I can point and say that any one of these is definitely more important, but the collection of those things is what’s really driving differences between children within the same family.”

Birth order — the idea that your age relative to your siblings plays a role in shaping certain aspects of your psychology — has traditionally been a topic of heated debate among evolutionary and developmental psychologists. Its reputation for arbitrary and anecdotal evidence perhaps hasn’t been helped by the fact that one of the earliest proponents of birth-order effects was the Victorian “father of eugenics,” Francis Galton, who noticed that an unusually high number of his fellow high-achieving “English Men of Science” in the 1870s were firstborn sons. For a more modern, less problematic equivalent of Galton’s observations, much is often made of the fact that of the 29 astronauts who flew NASA’s Apollo missions between 1968 and 1972, 22 were the eldest (or only) child in their families.

In fact, while a lot fuzzier than genetic studies, there is plenty of firmer evidence to suggest that some patterns in personality (many of which impact on attitudes to money) among firstborns, middleborns and lastborns can be discerned. In a 2014 study, for example, Feifei Bu of the U.K.’s University of Essex found that eldest children have a statistical advantage over younger siblings when it comes to education — “specifically that firstborns tend to achieve a higher educational level than their later-born siblings,” putting this down to a generally more motivated personality. “The advantage of firstborns in educational outcomes may be partially explained by the fact that firstborns tend to have higher aspirations which push them toward higher educational levels,” Bu wrote.

A more recent study, meanwhile, has suggested that only-child status increases people’s likelihood to play the stock market, while economic research by Sandra Black at Columbia University has shown that in the mid-2000s people’s average earnings reduced incrementally (by a percentage point or two) depending on whether they were first, second or third children — and that this effect was more pronounced for women.

Siegel, together with a colleague at Imperial College London, has recently conducted his own research into birth-order effects that seems to back up the idea of a cognitive edge for the eldest. “We reversed it a bit, so we were mainly interested in whether or not CEOs are more likely to be firstborns,” he says. “Even though our data are somewhat imperfect” — since they didn’t look any further down companies’ hierarchies than the chief-exec level — “we do find evidence that indeed CEOs are much more likely to be firstborns than not.”

Other studies focusing on personality traits have found oldest siblings to be more risk-averse than their younger brethren, which might explain their apparent success with attaining status and could signal a more circumspect attitude to money.

The classic of the birth-order genre is Frank Sulloway and Richard Zweigenhaft’s 2010 investigation into relative risk-taking by pro-baseball-playing brothers. Poring over the stats of Major League history they found that, of 90 pairs of brothers, the younger siblings, regardless of talent, consistently tried to steal bases more often than their older pro bros. “We often look at it in terms of physical risks,” says Salmon, “but investment risk is another way that people can look at it.”

Invoking an evolutionary perspective, she suggests that this aspect of birth-order psychology could stem from a time when resources were scarce, and siblings had to compete with each other for food and parental attention (which often might have amounted to the same thing) in a more direct and brutal way than in today’s societies, where families usually have more of that stuff to go around. “You might see those kinds of differences because later-borns are inherently more willing to take risks,” she says, “whereas firstborns already have a certain position and there’s a tendency to not want to risk the things they have.”

“A sibling can be your closest ally but can also be your closest competitor,” she adds, and this primal competition for space in the nest and to be first to grab food out of mom and dad’s beaks might explain why “you see so many stories in mythology that focus on conflicts between siblings — even though you see people value sibling solidarity. You also have stories from mythology and the Bible about siblings trying to off each other.”

According to Salmon, those early squabbles over toys or the last slice of pizza tend to be more intense when siblings are closer in age and when they’re of the same sex. Combined with birth-order effects nudging siblings into different strategies, this may lead to more striking differences when it comes to possessiveness and resource allocation later in life. “There’s a certain way you view the world, or strategies for how to get what you need, that form relatively early,” she explains. “If they consistently get reinforced all the way through childhood, you often will use those same strategies when you leave it. Sometimes they may work and sometimes not, and sometimes people will modify them when they’re adults (because it’s not like we’re fixed in stone from that point on). But they certainly flavor people’s approaches to things; they sort of absorb this view of the way things work, and they take that outside.”

Am I My Brother’s Record Keeper?

“Really what we mean when we’re talking about birth-order effects is a focus on two separate aspects,” says Salmon, which can combine to pull siblings in different directions. One is competition between siblings for all the attention, love, leeway and good stuff that flows from their parents. The other, she says, is that parents themselves will tend to “differ in how they invest in each of their kids, or in the types of attention and investment they give to their children.” This variation in how each kid down the line gets treated can set up different benchmarks they feel they need to work toward.

“Children are interested in maximizing their own investment from their parents,” Salmon explains, “and for firstborns that often means fulfilling parental expectations. That can lead people to go into the family business, to become a doctor, for example, or to follow the same kinds of occupation as the parents.” For later arrivals to the family, the parental investment might not be felt so intensely, so the urge to follow in footsteps “may be different for children that don’t have the same parental expectations and in some sense are more free to figure out whatever they’re interested in and just do it.”

This constellation of push and pull factors offers another possible explanation for the wide variation in monetary policies within families. Particularly for middle- and later-born children, the competitive need to differentiate themselves from their elder siblings might present a strong incentive to willfully adopt different approaches to life. The phenomenon known as “deidentification” will be familiar to anyone from a home where bickering siblings take every opportunity to harp on what makes them different from their brothers and sisters.

“To the extent that if you’re trying to attract parental attention or make yourself valuable within your family group, being different than a sibling is a useful thing,” says Salmon. “If the first boy born in a family is a tremendous athlete, and you come along four years later, competing on the same level, they’re already bigger, stronger, have advantages in that area. In many cases your best route might be to go the exact opposite way and be a computer programmer — to have interests that are very different.”

It’s why one sister who is seen as responsible with her savings or diligent in her job might have unknowingly inspired a younger sister to swerve her life onto a less striving, happy-go-luckier heading. “That effect is probably stronger in families where you have same-sex siblings,” says Salmon, “because they need to make themselves more different. If you just have a boy and a girl, they’re often different anyway — parents react to them differently without meaning to.”

Hormonal Hermanos

Opposite-sex siblings might also be driven toward different life strategies while they’re still in the womb — regardless of how their genes match up. While Siegel is unsure about a direct link between birth order and risk-seeking behavior (in a recent paper he points out that “empirical support for the association between birth order and risk preferences is mixed”), he has found evidence to suggest that an individual’s risk tolerance can be dictated by another aspect of their biology.

“In yet another paper using the Swedish twins,” he says, “we looked at prenatal testosterone exposure.” He points to a punchy line of research pursued by others that shows people’s appetite for risk and aggression on the trading floor rises with the amount of testosterone circulating in their systems — what he and Cronqvist term “the masculinization of financial behavior.” “We tried to look at whether or not your brain is built slightly differently if your dosages of prenatal testosterone are higher,” he explains. “And we do find some evidence that that is the case.”

Since levels of testosterone exposure can vary significantly from one pregnancy to another, and is thought to have differing downstream effects on female versus male children, this could be yet another environmental source for siblings’ divergent outlooks and prospects.

Both Siegel and Salmon are careful to point out, though, that all of the above by no means exhausts the list of “non-shared experiences” that might account for deviating pecuniary profiles. As well as birth order, genes and hormone levels, Siegel cites siblings’ contrasting memories of living through economic crises in their early years as another potential fork in the road, as well as their changing attitudes to risk as they react to the unpredictable personal events in their lives.

He also says that the cause of parental influence isn’t lost. For moms and dads keen to impart their financial wisdom for a healthy return on their offspring’s prospects, “We actually do find that in settings where the parents are better off financially or where there are fewer (non-twin) siblings in total, the parental effect does get stronger.” This, he says, is consistent with previous research that has been done on parents (again in Sweden) who have adopted their children — so in this case the genetic link to personality traits is removed from the equation. In these findings, “the adoptive parents are much more important than our results would have suggested,” says Siegel, acknowledging that this opposite methodological extreme from twins research challenges some of his own conclusions. So, he concludes, “We’re not quite at the end of where to draw the line. Both sides find evidence of nature and nurture; we find more nature, they find more nurture.”

And it’s worth remembering, as Salmon cautions, that while sisters’ and brothers’ attitudes and preferences might seem as distant as those of perfect strangers across a whole range of topics in life, “there are also siblings who have a lot of similarities on those things as well. And so, to me, what ends up being different is often strategies. They just take different approaches to getting what they want. Even though sometimes they may value some of the same things, they may go after them in different ways. Everybody wants to succeed, but of course not everybody always succeeds to the same level, because there’s luck and there’s just inherent differences between people.”

Whatever the incompatibilities within families, it’s worth remembering that while a brother or sister’s lazy or wasteful or too cautious or overly ambitious life choices might seem weird or wrong-headed to you, there’s no reason at all that their priorities should ever match yours. In fact, there are a thousand reasons they shouldn’t, whether you grew up under the same roof or not.

So it’s maybe worth extending a fair amount of forbearance to those unwise money decisions they’re always making. As Salmon points out, “Sibling relationships are really formative and they’re really important because they’re also with you for the rest of your life. Your parents are there, but then they aren’t there typically at the end. Barring things like unforeseen illnesses, parents aren’t with you forever. But your siblings usually are. For better or for worse, right?”

And, of course, for richer or for poorer.

Chris Bourn

Chris Bourn is a writer and editor who has writed and edited for many a title, including British Maxim and Time Out. He does stories for MEL covering health, happiness, and how things came to be.