Student loans are the financial equivalent of Marvel movies: insanely expensive, aggressively expanding and seemingly unavoidable. The class of 2016 will carry the highest average student loan debt ever, with 7 out of 10 seniors graduating in debt. And the average debt load is $37,172 — up from last year’s (previously record-breaking) $35,000. According to the Wall Street Journal, the size of all student debt has tripled over the past decade. Student loans are now the second-largest source of personal debt in the U.S.—more than credit card and auto loan debt, and trailing only mortgage debt.

In case this isn’t daunting enough, even these enormous figures may be understated, as colleges may not account for the private loans students take out. (Nationally, nearly 20 percent of all graduating seniors’ debt came from private student loans.)

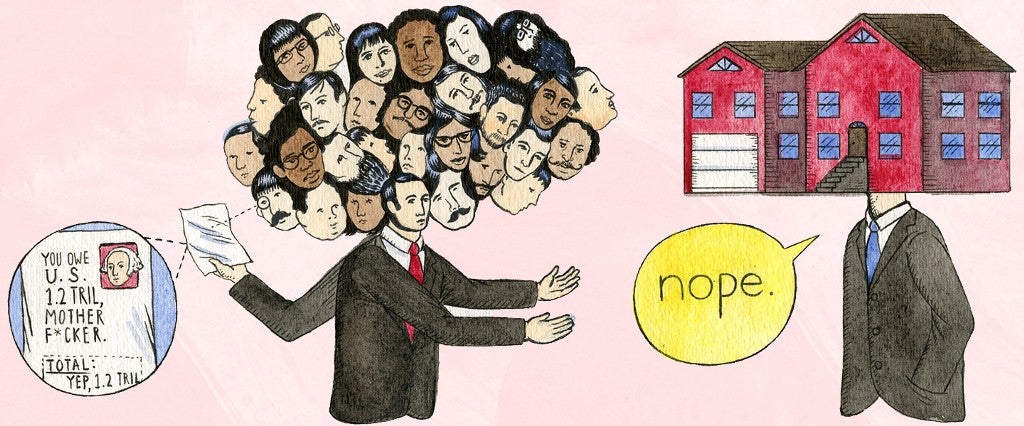

With about 40 million Americans on the hook for some enormous loans, one question naturally arises: What would happen if we didn’t pay them back?

On a personal level…

Before we examine that grand scenario, it’s worth looking at the consequences for just one individual who refuses to or cannot pay back student loans.

You’ll get deeper in debt.

Interest will accrue and your balances will grow even larger. Loans that go to collections will incur additional collection costs of up to 25 percent.

Your credit score will suffer.

Late payments will appear on your credit reports and your credit score will drop. Negative information may be reported for up to seven years.

You’ll eventually go into default.

Most federal loans are considered to be in default when a payment hasn’t been made for 270 days.

Private loan lenders don’t have the same collection powers as the federal government, but they can sue the borrower. If a suit is successful, they can use whatever means are available under state law to collect the judgment.

Kiss your tax refund goodbye.

If you have a federal student loan in default, the federal government may intercept your tax refund. Married filing jointly? Your spouse’s portion of the refund may be at risk too. (Private student loan lenders can’t intercept tax refunds.)

Your wages may be garnished by the government.

Up to 15 percent of your disposable income. Gone.

Any co-borrowers are in as much trouble as you are.

Anyone who co-signed a student loan for you is on the hook 100 percent for the balance. (Sorry, Mom.)

You may be sued.

Lawsuits are less common with federal loans than with private ones. (Why sue when the government has so many other ways to collect?) But a lawsuit is always a possibility.

You’ll be haunted by this debt until you die.

There is no statute of limitations on federal loans, which means there is no limit on how long you can be sued. It’s like contracting financial herpes (except you never even got to have sex).

On a national level…

Here’s the fun part: If 40 million Americans were to decide, “Fuck it, we’re not paying.” Below are some possible outcomes:

- Immediately, 40 million Americans would lose pretty much all ability to buy a house through a mortgage or open a credit card without paying usurious rates for either. This could wind up depressing the housing market, causing a ripple effect for many other industries that depend on housing (speculators and banks might face the brunt of it).

- The lack of credit could cause a consumer-driven credit freeze similar to what we saw in the 2008 crisis, but caused by lack of short-term debt instead of housing prices going down (although we might get a fair bit of that, too, from the housing issues).

- Only 6 percent of student loans are held privately, but 6 percent of $1.23 trillion is still a ton of money. Those lenders might go bankrupt or need federal assistance. Ultimately, we can imagine the federal government “eating” the loss on these loans, which might irreparably harm the government’s credit rating.

- If the U.S. government’s credit rating were to falter, we could wind up in a situation where interest rates suddenly go up and the government’s ability to borrow gets constrained. Then we might wind up in a Japan-esque lost decade scenario, in which the interest payments for our government debt far exceed the rest of our annual budget.

- In that crazy case, the U.S. government might default, not unlike what happened to Russia and/or Argentina.

And finally, on a global level…

Going further into the realm of extreme possibilities:

- If the U.S. were to default, then China’s entire model of “repressive single-party government that keeps the populace in line because of strong economic growth every year” will be in even greater jeopardy. (China’s growth has already faltered). They are trying hard to reduce their dependence on external consumption, but for now, they are still inextricably tied to U.S. consumption. It might be crazy, but China’s best move might involve bailing out the US. Basically, it’d be almost exactly like Super Sad True Love Story.

- Another extreme possibility: After the bailout, we’d still have to cut huge swaths of our budget, which would mean we’d lose a significant portion of our defense budget. Consequently, we’d lose a significant portion of our power projection in the world, allowing China to have more of a hand in Middle Eastern affairs and creating regional power vacuums that Russia and ISIS could fill.

- So in addition to having a lost-decade-esque, Depression-stricken country, where no one could afford to buy anything (or even have the credit to buy things they couldn’t afford), Vladimir Putin, China, and “the terrorists” would radically change the geopolitical landscape.

So pay back your loans, or the terrorists win.

Panio Gianopoulos is the author of A Familiar Beast and the editorial director of Heleo.

- Into the Black: How I Cut My $118,000 Student Loan Debt in Half

- Why Do People Spend More Than They Make?

- Show Me the Money