When I wasn’t paying my student loans—leading them to go into collections—I constantly felt a palpable sense of terror. It was a dread that only felt a little worse than how I feel now when I actually pay them. Apparently, I’m not alone. Not only do 40 million other Americans have student loan debt, too — to the tune of $1.3 trillion overall — studies show most of us feel a sense of guilt, shame and emotional burden regarding those loans that affects us differently than other kinds of debt.

Interestingly, though, it’s something more and more employers want to help out with — essentially paying down your student loan debt for you so you can be less stressed about it (and ultimately, be a better, more productive employee).

That’s the thinking behind it at least.

The concept isn’t limited to Silicon Valley or other progressive industries when it comes to compensation and company culture either. In the last couple of years, Chegg, PricewaterhouseCoopers and Penguin Random House have all instituted student debt repayment programs. And while all of those programs definitely have their own merits, I was most intrigued by what Fidelity is doing in this regard — because it hasn’t just instituted a repayment program for its employees, it’s begun to work with other companies to implement similar programs within their benefits packages.

And so, I recently reached out to Asha Srikantiah, the Head of Product for the student debt program at Fidelity, to discuss why the program was created; how it works; and the new responsibility of employers to make up for our overall lack of financial literacy.

What is the origin of the Fidelity program?

Three years ago, we started exploring the problem of student debt from within an internal research and development group we have called Fidelity Labs. We started to hear from employees that student debt was starting to get in the way of some of the goals, hopes, dreams and conveniences they wanted. We also started to hear a few things in the media about this. Similarly, every year, our CEO Abby Johnson does a listening tour across all of our nationwide sites, and during these tours, she kept hearing that student debt was a big sticking point in our employees’ lives. So Fidelity Labs began exploring the topic in greater depth.

A lot of the way we work here is inspired by start-up style methodology. In other words, we learn by sharing prototypes and having people give us feedback. As such, we started to develop a fleet of products that could help people with their student loan debt. One of those products is the Student Debt Tool, an online platform that helps people who currently have student loans begin wrapping their head around the problem. This is so important because of the emotional burden of student debt. That’s rooted in the fact that for a lot of people, their student loans are the first thing they’ve ever had to deal with within the realm of personal finance.

Our second product is a student debt employer contribution program that we initially created for our own employees. Abby told the human resources team, “Hey, this is a problem that we need to help our people with. We should be putting money where our mouth is within the space and help our employees navigate this financially.” This was brand-new to the market, but Abby and our HR team thought such a program would help us with recruitment and retention.

How exactly does the program work? Do your employees select this program instead of another part of the benefit package? Does it have any effect on what they get for a retirement?

Fidelity provides $167 every single month, with a total amount of $10,000 over the course of five years that gets paid directly to an individual student loan. None of the employees at Fidelity have had to choose between drawing down on this benefit versus any other benefits that are offered, and they aren’t earning any less because of their participation in the program. We offer this in addition to the other benefits we offer.

When the program began, literally hundreds of our current clients in the 401K space called us up and asked how they could be more involved with what we’re doing with student debt. So that’s our third product — or the third leg of the stool, if you will — which is broadly offering this type of benefit to clients. We implemented it ourselves, and now we’re pushing it into market. To that end, we already have several clients working with us to provide the same type of benefit to their own employees.

Do you think employers have a responsibility to help their employees with overall financial literacy?

Well, in the conversations leading up to us creating these programs, one of the recurring themes was people saying they wish they knew more when they were in high school and during the decision-making process of choosing a college. Financial literacy isn’t formally taught, and it’s not innately learned. That’s why the Student Debt Tool was created as an online education platform to help people, first and foremost, face their own loans. You enter your loan information, and then the information is presented back to you in a way that’s easy to understand. It empowers you to say, “Okay, I have options.”

What has the response from employees been like?

We had overwhelmingly positive responses from our employees immediately, including employees who didn’t even have student loans. It was a morale booster across the board. And looking at the data from the last couple years, we see that it’s improving both recruitment and retention across the board.

Why do you think people feel differently about student debt than they do other sorts of debt?

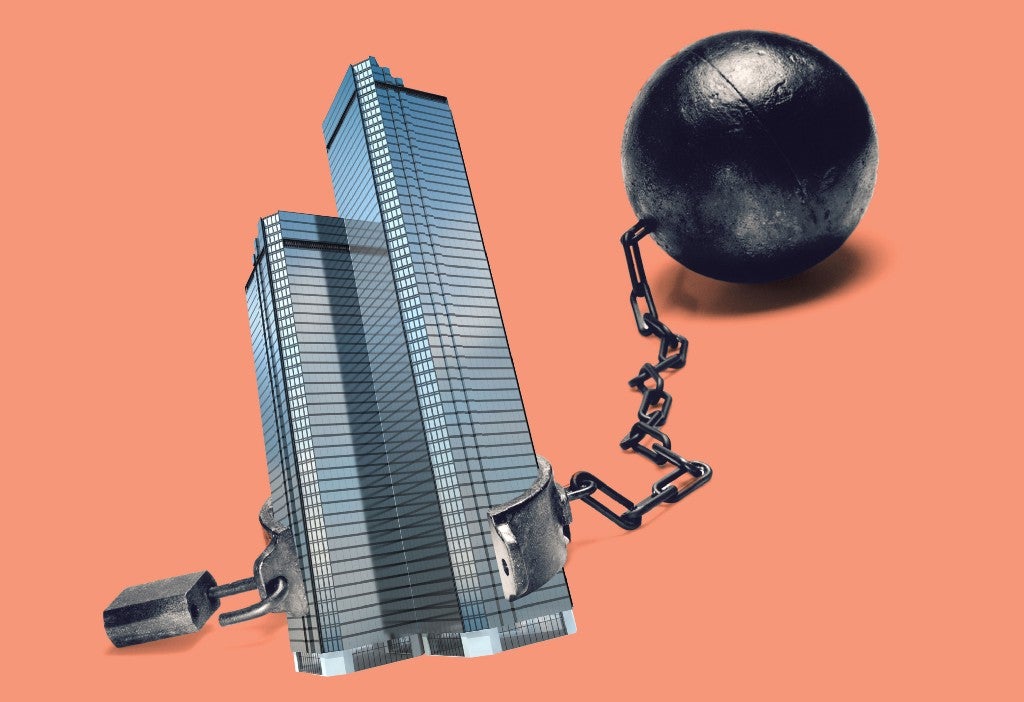

I’ve had countless conversations with people of all ages with student debt, and there are a couple of different emotions that I’ve heard over and over again. Student debt is a ball-and-chain that people feel drags them back to a time in their life that’s in the past, not right now. The name “student debt” reinforces that, giving it a negative connotation related to school years after someone’s graduated. While these people are grateful for the education their loans afforded them — and all the steps they’ve been able to take as a result of that education — it seems people resent their student loans in a unique way. Paying your mortgage feels like a step toward one’s future, while student debt makes them feel stuck in the past.

We assume student debt is a a young person’s issue, but when you’re talking about employees feeling like their loans are an issue preventing them from having savings or certain kinds of securities and comforts, I’m assuming you’re not just talking about people fresh out of school.

It’s easy to think about student debt as a millennial problem, but student debt is truly a multi-generational issue. Fidelity’s 401K customers are a broad representation of the American workforce. We surveyed them and found that over one-third of our current participants currently have student debt. There are definitely more millennials — 63 percent — but 36 percent of Gen-Xers have student debt, too. So do almost a quarter of Boomers. And almost 80 percent of folks we surveyed across generations said student debt is impacting their ability to save for retirement.

Fidelity is also figuring out ways to better help pre-college families who are navigating the college decision process in regards to their children. We hope to bring more transparency into those conversations and make people feel more equipped to think about what they’re signing up for at the onset of their student loans. We want to help families with young kids plan for this, too, because if the growth of education prices continues at the rate it has been, people who have young kids now are looking at having to pay an extraordinary amount to fund their kids’ education in the future.

I feel like your program exemplifies the blurring of the lines between one’s professional and private life. Like, in the past, I don’t feel like most employees would’ve been comfortable even sharing information about their debt to their employers, let alone partner with them to pay it off. Do you think that’s accurate?

We’re definitely seeing a tremendous shift in the way our “work lives” and the rest of our lives bleed into each other — and depending upon where you work, your work life may become your social life.

A lot of employees now are looking to their employers for help and guidance with things that were historically considered to be very personal, like finances. The whole topic of financial wellness in the workforce has come up in major, major ways. It’s because in a lot of situations, employees don’t know who to turn to or who to trust, and you’re already spending so much of your daily life with your employer, why wouldn’t you turn to them for some of these topics that you need help with?

That’s at least what we’re starting to see — employers being asked by their own employees to support them in all sorts of ways, whether it’s financial wellness or actual health and wellness.

Tierney Finster

Tierney Finster is a journalist, screenwriter, actor and model from Los Angeles, California. She is a contributing writer at MEL, specializing in love, sex, mental health, drugs, queer culture and the cannabis industry. She has written for publications such as Playboy, Purple, Dazed and Confused, Jezebel and Broadly and was the key researcher behind Sex On, HBO’s revival of its iconoclastic docu-series Real Sex.