I saw a post on Reddit’s super-popular personal finance forum earlier today that made my eyes bleed and my heart cry.

“Friend declined pay raise because he’d ‘make less money,’” the post reads. That much is pretty self-explanatory, but to briefly summarize: A man relays the story of his friend, a presumably good-hearted but nonetheless foolhardy man who turns down a raise because of the false impression that he’ll actually earn less because of an increase in his tax rate.

I’m here to tell you that this fellow is wrong. Terribly wrong. And that’s distressing.

Even more distressing is that I see this kind of argument with regularity lately, probably because the Trump tax plan has made people generally more aware of our country’s Byzantine tax system.

But that general awareness hasn’t translated into a nuanced understanding, as this Reddit post shows. If anything, the misperception about how our tax system works is shockingly common, says Robert Weagley, chairman emeritus of the Personal Financial Planning Department at the University of Missouri. “When I was teaching personal finance, the students had a lot of trouble getting their arms around the tax system, especially the concept of marginal tax rates,” he says. “It’s only on the incremental income that a person is being taxed more, and that’s only if they’re on the cusp of a new tax bracket.”

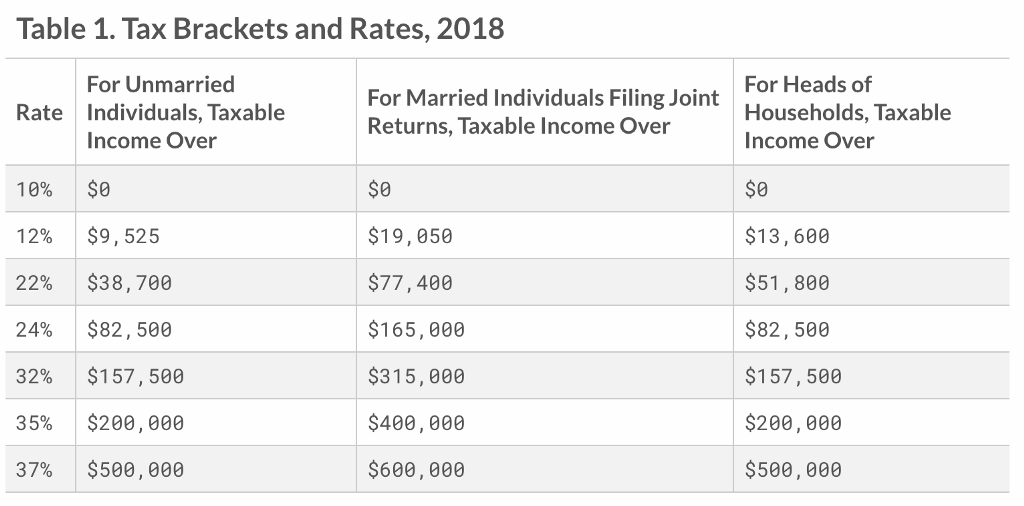

That can be a tough concept to understand, so let’s look at in terms of real numbers. Here’s a look at the tax brackets for 2018 under the new Republican tax plan (courtesy of the Tax Foundation):

Say a person is single and earning an annual income of $150,000. Contrary to what many believe, that doesn’t mean the person pays a 24 percent tax on all $150,000. They pay 10 percent on the first $9,525 they make; 12 percent on the income they make between $9,525 and $38,700; and 22 percent on their income from $38,7000 to $82,500. They only pay a 24-percent tax rate on the last $67,500 of their income — or the money they earn over $82,500.

Now, say that person is offered a $10,000 raise. Yes, that would push them into the 32-percent tax bracket. But the first $7,500 of that additional cash will still be taxed at 24 percent. It’s only they money they earn above $157,500 (the remaining $2,500) that would get taxed at 32 percent.

Some people believe that earning a higher salary will hurt their take-home pay because it will decrease their Earned Income Tax Credit. But that’s only partially true. Yes, a person’s EITC decreases the more money they make, but it decreases gradually. And the decreases will never be so great that they will offset the increase in income a person would get from a higher salary, according to Andrew Zumwalt, professor of personal finance at the University of Missouri.

The only time a raise might be somewhat harmful is if a person is on food stamps or similar government aid program, and increasing their income would disqualify them from those benefits. (Conservatives often refer to this as the “welfare cliff,” and use it to argue against entitlement programs.)

But those scenarios are exceedingly rare, and don’t apply to the overwhelming majority of people eligible for a raise. Even on the off-chance that a raise would hurt a person financially, the temporary setback would be more than offset by the positive, long-term effects of getting that raise. A higher salary allows you to negotiate a better salary at your next job, or during your next job promotion. So leaving a raise on the table can drastically decrease your earning potential for years to come.

Reporting on personal finance is often a depressing reminder that most people know absolutely nothing about how money works, let alone how to effectively manage it. But nothing is quite as disheartening as hearing about well-meaning people turning down a raise because of the false belief it will somehow hurt them financially.

As Zumwalt says, “It’s a marginal system, you can’t lose money by making more of it.”