Several weeks ago, I got accepted into Your Money and Your Life, a private Facebook group moderated by NPR that’s for sharing personal finance tips and questions. And earlier this week, a woman who simply goes by Amy Mary asked the group: “What is your money personality?”

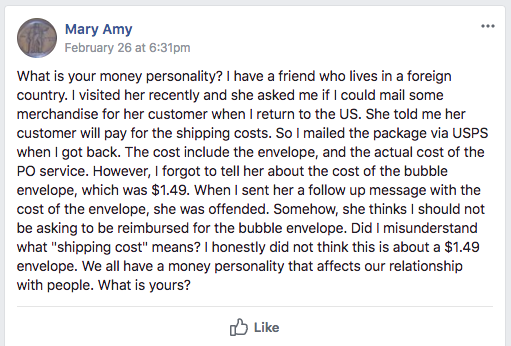

Mary had gotten into a tiff with a friend over a measly $1.49. Petty as the argument may have been, Mary was technically in the right. She sent her friend a package with the understanding Amy would be reimbursed in full. Amy got paid, but she later realized she forgot to include the cost of the envelope. However, when Amy Mary asked for an additional $1.49, the friend was aghast. It appeared the friends had fundamentally different money personalities.

Back at Your Money and Your Life, everyone looked right past Amy Mary’s money personality question and instead got into an endless, bad faith debate about whether she was right to ask for the money — completely true to form when it comes to online discourse.

Which is a shame, because an honest assessment of one’s money personality is precisely what most people need.

The “money personality” idea has been gaining traction over the past year, with more and more personal finance advice sites urging visitors to identify their distinct financial temperament.

It still isn’t a common term, but it should be, because it acknowledges that a person’s relationship with money, and their skills at earning, saving and investing it, are in inextricably connected to who they are as a person — their attitudes, behaviors and lifestyle; their strengths and weaknesses; their admirable qualities and irrational ones.

Personal finance guru Dave Ramsey likes to lump people into one of two personality types: Nerds and Free Spirits. Free Spirits hate rules and restrictions, and thus, they tend to spend frivolously and have trouble sticking to a budget. Nerds, on the other hand, crave order, and get their dweeby rocks off by making elaborate Excel spreadsheets that track every cent, and ruthlessly adhering to their budgets.

To me, though, Ramsey’s taxonomy is too rigid, especially for something as nuance as personal finance. Much like gender or sexuality, money personalities aren’t binary — they’re a spectrum.

For instance, fellow MEL staff writer Tracy Moore and I frequently debate whether a person should spend money on coffee. I’m decidedly in the no camp — people should avoid spending $7 on a coffee (whenever possible), and instead, drink the shitty office coffee when they get to work. And I get unreasonably frustrated when I see entitled millennials who scoff at the idea that not buying Starbucks will have substantial impact on their financial health. (We can call these people the Defiantly Financially Illiterate.) The truth is, cutting $5 out of your daily spending can mean the difference between retiring comfortably and working until you’re on your deathbed.

Tracy, meanwhile, thinks that coffee is a necessary expense. The ritual of waking up, breathing in the aroma of the local coffee shop and getting a freshmade cup of joe is among the little pleasures that makes life worth living. It’s a much-needed respite that helps people maintain their sanity and continue functioning at a high level.

The truth is neither of us is right, and neither of us is wrong — we just have different money personalities. My money personality is to save on needless food spending so I can do activities I enjoy, such as traveling or going to concerts. But for Tracy, drinking coffee is a necessity. She limits her spending in other areas, so she can enjoy professionally made coffee. We both believe in living within your means, but execute that plan differently. She’s the Coffee-Haver, and I’m the Coffee-Eenier.

Amy Mary says she came up with the term “money personality” herself, as a way to better understand her fellow humans. “It was a loosely coined term,” she tells me. “I like understanding people, and categorizing people by their Myers-Briggs personality type has helped me in my personal relationships.”

Most people just trolled her for being cheap, but she did get a few useful answers. One man (The Friends Before Finances Guy) said he wouldn’t have bothered to ask for the $1.49, because he values friendship more than money. Another (The Time-Saver) said $1.49 isn’t worth his time — in the eternal balance between time and money, he always values the former more than the latter. (Indeed, spending money to save time has been shown to drastically increase a person’s happiness.)

For her part, Amy Mary identifies as Frugal but Entrepreneurial. “I’ve never needed a fancy car or house, but I’ll spend if I see the potential for making money.”

Other money personalities I’ve encountered are The Habitual Overspender, The Sensible Shopper and The Defensive Non-Saver, the guy who makes no effort to secure his financial future and resents when people urge him to do otherwise.

Not that they can’t change. Like other parts of their personality, their money personality is mutable and liable to evolve over a lifetime. I, for one, used to be a Scrooge, living a life of extreme austerity (and extreme isolation). (Some people call this money type the Hoarder.) It was only with time that I learned I’d be happier if I eased up a bit, and spent just a little bit of my hard-earned money on recreation.

So these days, consider me a Reformed Scrooge — and a lot more fun to be around. I’m still, though, working my way toward a Reformed Scrooge Who Will Pay for Coffee Instead of Making the Shitty Kind Himself.