In 2013, University of Chicago economist Harold Pollack achieved viral fame when he claimed that all the personal finance advice a person needs could be neatly summed up on a single 4×6 index card. The card’s wisdom, written in Pollack’s slightly messy script, included some rather technical advice: “Buy inexpensive, well-diversified mutual funds,” “Avoid actively managed funds” and “Maximize contributions to tax-advantaged savings vehicles like Roth, SEP, and 529 accounts.”

But two lines on the card were simple enough for anyone to understand: “Save 20% of your money,” and “Pay your credit card balance in full every month.”

Don’t spend more than you earn.

It may be the most basic and yet the most routinely flouted rule of personal finance. People just can’t keep from spending more than they bring in, forcing them to dip into savings, borrow money or go into debt.

The problem particularly affects low-income Americans. Last year, poor families in the U.S. — those in the bottom 30 percent of the income scale — spent, on average, almost twice as much money ($25,000) as they brought in ($14,000). They also spent a higher portion of their incomes on housing, transportation and food than did middle-class and rich families. It is, as the saying goes, expensive to be poor.

It's very expensive to be poor. #2020Approach

— Bernie Sanders (@BernieSanders) November 21, 2015

But it isn’t just the poor who spend more than they earn. The Federal Reserve’s “Report on the Economic Well-Being of U.S. Household in 2014,” released last May, paints a dismal portrait of the nation’s current and future financial health. Almost a quarter of American households underwent some form of financial hardship in 2014 — such as a costly medical emergency or unexpected job loss — “and the results demonstrate that households throughout the income distribution struggle to maintain a financial safety net that could minimize the repercussions from such events,” the report reads. “[Thirty-one] percent have no retirement savings or pension.” While 63 percent of survey respondents reported having saved some money in the past year, 20 percent reported that their spending exceeded their income across all income levels. And a staggering 15 percent of respondents who earned more than $100,000 per year spent more than they earned.

It’s more than mere money that causes people to overspend — it’s poor financial decision-making. Which raises the question: How and why do people rationalize the apparently irrational decision of spending money they can’t afford to part with?

In short: Americans have a YOLO problem. Our obsession with the immediate clouds our judgment of the future, allowing us to justify irrational expenditures by ignoring their long-term impact.

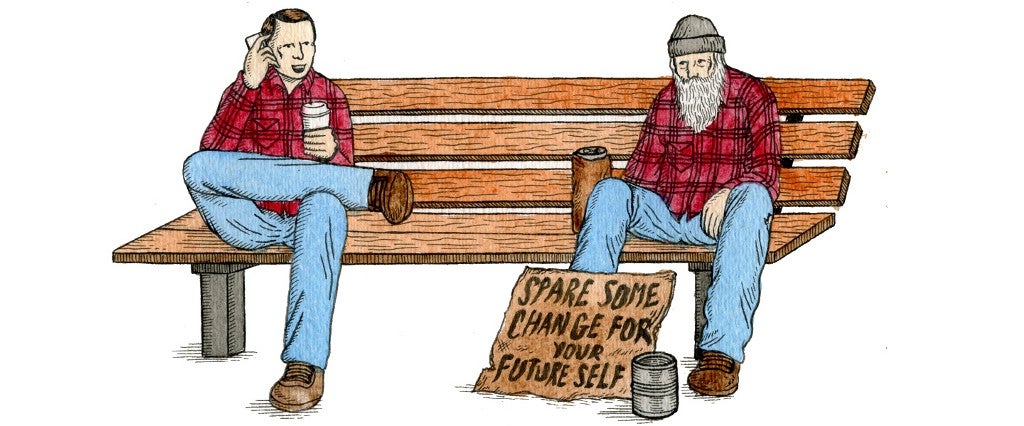

“People are, for whatever reason, valuing the present more than the future,” says Abigail Sussman, assistant professor of marketing at the University of Chicago’s Booth School of Business. This phenomenon is an aspect of “intertemporal choice,” Sussman says, which states that the less we spend today, the greater our consumption power in the future. It sounds obvious, but its impact can be immense. Financial self-help guru David Bach once noted that 20-somethings could become multimillionaires by retirement if they stopped spending $5 a day on Starbucks and put that same amount into a 401(k) or IRA.

Problem is, most people feel estranged from their future selves. “Some people think about the person they are in retirement, and it doesn’t remind them of themselves,” Sussman says. And the thinking becomes, I’d rather spend the money myself than give it to some stranger.

This disconnect between our present and future selves is supported by a recent UCLA study. “When people think of themselves in the future, it feels to them like they are seeing a different person entirely … like a stranger on the street,” UCLA psychologist Hal Hershfield says.

Sussman points to research conducted by her colleagues Daniel Bartels and Oleg Urminsky, who found that shortsightedness was not the only problem. Even when people considered the ramifications of their present-day consumption, they vastly underestimated its long-term consequences, leaving them prone to frivolous spending.

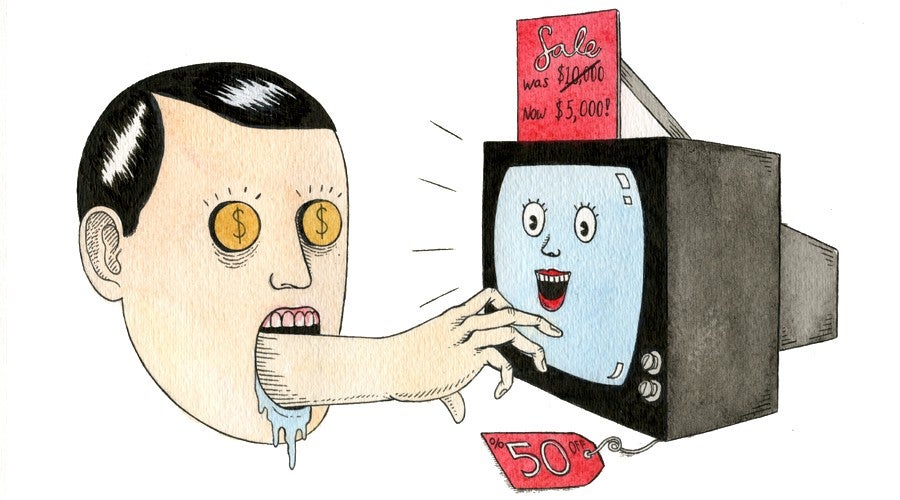

Other factors also contribute to the overspending issue, such as poor impulse control — seeing a TV on sale for 50 percent off entices us to buy, regardless of whether we can afford it — and a general lack of financial literacy, particularly about the impact of compound interest, Sussman says.

Compound interest — the interest earned on interest — causes savings to increase exponentially. But “most people think their money will increase in a more linear way,” Sussman says. So when it comes time for you to decide between buying that coffee or stowing the money away, “you’re not making an appropriate cost-benefit analysis, because you don’t understand the benefit [of saving], but you do understand the cost.” Next thing you know you’re plunking down $880 on a three-day VIP pass to Coachella even though you promised yourself you wouldn’t.

“Compound interest is only your friend if you start investing early,” says Daphna Oyserman, a psychology professor at USC’s Dornsife Center for Mind and Society. “We are wired to focus on right now.”

Oyserman says our focus on the immediate is an evolutionary impulse — our Cro-Magnon ancestors were too preoccupied with not being eaten to contemplate target date funds, so now we, too, tend to concentrate on present matters.

Given the problems this can cause, Oyserman and her colleague conducted an experiment to see if they could make people think more urgently about the future. Subjects were asked to imagine their child attending college in the future and to concoct a savings plan. Half of them were told their child would attend college in 18 years, while the other half were told they would have 6,570 days to save. Subjects in the latter group planned to start saving four times sooner than their counterparts. Expressing the impending cost as a matter of days rather than years made the future seem more imminent; the need to save more pressing.

“Time is an abstract construct,” Oyserman says of the dissonance. “So time is translated into distance. A day is right now and for sure. But there’s distance between me and a year from now.”

Some believe Americans’ lack of savings, especially among young adults, isn’t as alarming as the numbers seem to suggest. But this position rests on the assumption that technology will allow millennials to continue working past 65, the traditional retirement age. That’s not so much a solution as it is a downgrading of expectations that would force an entire generation of Americans to work until their dying breath.

A better solution might be to use this grim prospect as motivation to change our spending behaviors today.

John McDermott is a staff writer at MEL, where he recently interviewed former NFL star Rashard Mendenhall about how scouts were skeptical of him for having interests outside of football.

More job and money from MEL:

- The Sons Who Didn’t Screw Up Daddy’s Family Business

- How to Send a Good Work Email

- Cider House Rules