The thought of someone putting their retirement savings into Bitcoin raises the hair on David Armstrong’s neck.

Armstrong is president and cofounder of Monument Wealth Management in Alexandria, Virginia, and to say he’s skeptical of Bitcoin (and other cryptocurrencies) as a retirement vehicle would be a gross understatement.

“Oh, geez,” he replies when I ask him about their viability. “[Cryptocurrencies] concern me. You could wake up one morning and all of your money is gone. I would not advocate that investment to any of my clients in any way, shape or form. You can’t see it. You can’t touch it. I don’t think that’s a prudent strategy for anyone saving for retirement.”

And yet, that’s exactly what thousands of Americans are doing now that Bitcoin, Ethereum and other cryptocurrencies have hit record highs in terms of value and mainstream popularity. More and more, people are looking at them as a lucrative component of a diversified portfolio, or in some cases, a singular alternative to traditional retirement savings vehicles.

Interest in cryptocurrencies has never been higher, says Chris Kline, chief operating officer of BitcoinIRA, a startup that (as the name indicates) allows people to roll their 401(k) savings into an investment in Bitcoin and other digital currencies. “When a product is moving, people take notice,” he adds

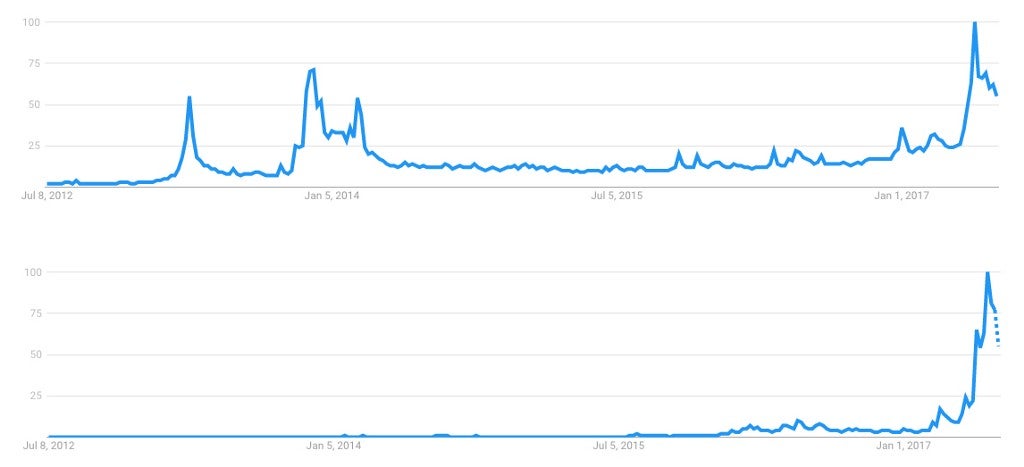

And move it has. Bitcoin exploded earlier this year, nearly tripling in price from March to June, and hitting a record high of more than $2,800 per coin on June 5, according to CoinDesk, a financial news site dedicated to cryptocurrencies. Ethereum, another cryptocurrency, saw its price spike from less than a dollar per ether last fall to $400 on June 13. Ethereum’s price has steadily declined since then—it’s at $268.28 as of this writing—but the profound price increases have piqued people’s interest in cryptocurrencies and given them some much-needed legitimacy. Google Trends data shows searches for Bitcoin and Ethereum are at all-time highs.

BitcoinIRA has been more than willing to capitalize on that interest. The company launched in June 2016 and now has more than 1,000 clients, with an average investment of $45,000, according to Kline. The company works just like a traditional, direct investment plan in that customers select where their money is allocated (as opposed to paying a wealth manager to make the decision). But the money is going into potentially volatile digital currencies instead of established investment options like stocks, bonds and securities.

BitcoinIRA is on track to take in at least $100 million in new investments this year alone, Kline adds. At a 10 to 15 percent service fee, that equates to at least $10 million in revenue for the young company. BitcoinIRA is also cashflow positive, which is virtually unheard of among most startups.

But Bitcoin as a retirement investment strategy remains a niche interest. It’s telling that most of BitcoinIRA’s clients live in metropolitan American cities with robust tech industries. And for old-school investment professionals, Bitcoin is anathema.

“No one has any idea how [Bitcoin] is going to perform over the long run,” says Robert Weagley, chair emeritus of the personal financial planning department at the University of Missouri. “I have confidence in the U.S. market in the long term. I don’t know if there’s going to be a market for Bitcoin six months from now, let alone 60 years from now.”

Armstrong is even more forceful in his critique, saying investing in Bitcoin is like putting all your retirement savings on black at the roulette table. “[Bitcoin] is just one of those things that seems very, very speculative, and anyone who does it has to realize that they could lose 100 percent of their money,” he says.

Kline acknowledges Bitcoin is risky. “It’s something we tell all our clients,” he says. But he says it’s not any less secure than the traditional banking system, which proved to be a veritable house of cards during the 2008 financial crisis. And unlike traditional investment firms—which slow down the exchange of money, and then charge their customers fees for doing so—BitcoinIRA allows customers total control of their investments for a 1o to 15 percent upfront fee, he adds. There are no extra charges for executing transactions or liquidating their investments.

Kline does not suggest that people put all their retirement savings in Bitcoin. Like almost all investment professionals, he advocates a diversified approach, with 5 to 25 percent going to Bitcoin.

Staunch Bitcoin proponents tend to have a libertarian, anti-establishment streak, and Kline’s arguments for it are in that vein. Bitcoin, he says, is a viable alternative to a corrupt banking system that overcharges customers instead of acting in their best interests, and is in cahoots with the very regulators responsible for policing them.

“When they bailed out the banks, did it help the little guy?” Kline asks. “It all got injected back into their businesses. The trickle down is not taking place.”

I asked members of r/Bitcoin, a Reddit forum for Bitcoin enthusiasts, what they thought of Bitcoin as a means to retirement. The answers I got were measured. Bitcoin proponents may have a reputation for being somewhat loony techno-libertarian types, but only a few of them advocate completely doing away with your Roth IRA and/or 401(k).

“Traditional retirement accounts have some benefits that Bitcoin does not offer,” writes Reddit user Stupidx (whose username belies his thoughtful response). The advantages of a traditional investment vehicle include no shaky legal status, a greater number of investment choices and a lower risk your invest will evaporate in an instant, Stupidx adds. “Bitcoin can go to zero. Compared to 401(k), Bitcoin has up until now offered much better rate of return, which is not at all guaranteed to continue.”

Indeed, Bitcoin has minted many multimillionaires who were brave and fortunate enough to invest in the cryptocurrency when it was still considered a passing internet fad. But the market can crash in an instant—and there will be no government bailout if it does. And that lack of security means many Bitcoin believers aren’t arguing that it should replace traditional retirement savings methods.

“Despite the potential for high profits in [cryptocurrency], I would counsel investors to first use traditional and more conservative investment options, up to the point where their retirement (and other) goals are fully funded. Then anything beyond that point can be invested in more speculative, high risk/reward options like cryptocurrency,” writes Reddit user Ebeliever. “If investments were plotted on a map in terms of risk vs. reward, out on the margin of the map would be Bitcoin.”