This past July, the Chicago Mercantile Exchange (CME) (known more simply as “the Merc”) shuttered nearly all its trading pits after 167 years of operation. And with it died the pit trader — an infamously lucrative, stressful job characterized by ruthless competition, fraternal camaraderie and the frenzied screaming and hand signaling among men (and a few select women) exchanging billions of dollars worth of commodities per day.

The pits dated back to 1848 when the Chicago Board of Trade (CBOT) established what would become the world’s first futures exchange. So-called “futures” contracts derived their name from their function — they were agreements between grain farmers and merchants to exchange a certain amount of grain at a future date for a particular price. Futures allowed grain farmers to know how much they could earn from their crops prior to harvesting, while merchants were able to lock in prices months in advance. Most importantly, it brought “price discovery” to the grain farming industry. Previously, grain farmers sold their crop yields independently and with little idea as to their actual value. The CBOT established a market rate for a bushel of grain, and a place where financial speculators could buy and sell futures contracts based on how they thought the price of grain — and later, other commodities — would fluctuate.

The CBOT diversified into other agrarian markets throughout the 20th century — in 1936, it began trading soybeans, and in 1968 it added its first non-grain-related commodity: chickens. Meanwhile the CME — previously called the Chicago Butter and Egg Board until it changed its name in 1919 — dealt in frozen pork bellies and live cattle, and later foreign currencies such as Deutsch marks and Swiss francs.

https://www.youtube.com/watch?v=-jHoE7Dn1uI&feature=youtu.be

The 1980s saw the introduction of “options,” contracts derived of futures. Options differed from futures in that they were not as binding: A futures contract stipulated you were going to buy the commodity for the given price at the given date, whereas options were binding to only one party (the seller). The buyer would pay a small premium for the option on a contract, meaning he retained the sole right to buy the contract at the agreed-upon price over a given period of time. If the buyer thought it advantageous, he would “exercise his option” on the contract, and the seller was obligated to sell it to him. If the option wasn’t exercised by the end of designated time period, the contract expired and no money changed hands (although the contract holder kept the premium).

Options drastically increased the complexity of the trading conducted on the floor and was the beginning of the end of a unique work culture (a trend exacerbated by automated trading).

Because unlike in New York, the financial epicenter of the world, the culture at the Merc and CBOT was decidedly blue collar. The prevailing image of a finance worker in the 1980s and 1990s was a WASP-y, East Coast Ivy leaguer from a prestigious family. Now it’s a computer science genius whose software executes thousands of trades in a fraction of a second. But many pit traders were from working class Irish, Italian and Jewish communities and were correspondingly hardscrabble.

They hailed from the city’s South Side Irish-Catholic enclaves such as Beverly and Mount Greenwood; North Side Jewish neighborhoods (e.g. Northbrook, Highland Park); and bougie nearby suburbs (namely, Evanston and Oak Park). The ethnic-religious makeup of the pits was reflected in the names of the largest firms that traded there: Rosenthal & Co., Lee B. Stern & Co. and The Goldberg Association; Hennessy & Associates, O’Connor & Co. and Cunningham Commodities. The joke was that the CBOT was predominantly Irish- and Italian-Catholic while the CME attracted more Jewish workers.

They were drawn to the pit not just because it offered the opportunity to make hundred of thousands (if not millions) of dollars, but because one didn’t need a college degree to get a job and excel there. The pits were distinctly American in this way — simultaneously professional and crude; cutthroat and convivial; an insular meritocracy governed by both greed and interpersonal relationships.

The death of the pit trader, then, is about more than the loss of a “work hard, play hard” culture, it’s emblematic of a troubling shift in the labor market at large: With jobs rapidly disappearing due to automation and a growing emphasis on computer programming skills, it’s increasingly difficult for high school (and many college) graduates to earn a middle class income.

MEL interviewed five CME/CBOT workers about their years in and out of the pits. And while their experiences varied, they all agreed on two things: There was no workplace quite like the CBOT and CME trading floors, and there never will be again.

- Dennis Alcock, 58 | Worked in the pits from 1980 to 2012, primarily as a broker-trader, executing trades on his own behalf and that of clients.

- Chuck Bohm, 55 | More than 30 years worked at various futures firms including Rosenthal & Co., MF Global and Wedbush Securities. He spent his later years working as an office broker in a client-facing role, as he admittedly didn’t have the stomach for the pits.

- Tom Carrol, 61 | A phone broker for 25 years, Carrol built and managed his own portfolio of customers for whom he executed trades.

- John “Lux” Lepkaluk, 61 | Worked 15 years in the pits, starting as a runner, then as a phone clerk, then a pit clerk and 10 years as a broker.

- Margery “Large Marge” Teller, 53 | Despite being a boys club, Teller was one of the most successful, well-respected traders on the floor. Known as “Large Marge” because of the massive amounts of money she put at risk, she worked in the pits for 20 years as a “local” until 2004 and retired for good in 2010.

A Foot in the Door

Jobs in the pits were heavily sought-after, so one often needed an “in” to get their start.

Chuck Bohm: This is a handshake business — you gotta know people [to get in and get ahead].

Margery Teller: I graduated from Brown in 1984 with an economics degree and was recruited for one job: clerk at O’Connor, one of the best options firms in the world. But I didn’t know it at the time — I just said, “Oh, a job.” The recruiter was a Brown graduate who wanted to hire women. The firm was 85 percent male, which actually was less men than the average firm.

CB: I started at the CME in the summer of 1977. I was 17. The guy who started Rosenthal & Co. was my second cousin, and one day his father just called me up and offered me a job as a runner.

John Lepkaluk: My best friend from school was working at the grain room in the CBOT, and he said, “You gotta come here. This is where it’s gonna be at.” That was 1976. But I couldn’t get in there—it was very Irish, and I wasn’t Irish. Luckily, my mother’s accountant’s brother was a clerk at Sal Stone, a firm there, and he offered me a job as a runner. I was just out of college, and went from earning commission as a stockbroker to making a couple hundred bucks a week. But I was willing to take a pay cut.

Dennis Alcock: I didn’t go to college. I was 22, working at my father’s gas station and I saw a commercial for the trading pit and I thought Wow. That looks badass. I wonder how they do that. I learned later that one of my buddies was on the floor. I told him, “Hey, if you ever hear of anything down there, let me know.” A couple weeks later I get a call from a desk manager at Stotler & Co., this grain firm back in the day, who says, “Put on a pair of pants, dress shirt and a tie and come on down here. No blue jeans.” I said “When?” He goes, “Right now, idiot.”

Tom Carrol: It was 1980. I was outside my apartment and saw my neighbor sunbathing. I asked him, “What do you do for a living?” He told me he worked at the Merc and it was the best job in the world. So I asked him how to get a job there and he said, “I’ll bring you there tomorrow. I’ll go down to the pit, make $200, then we’ll go golfing. How does that sound?” How can you pass up an offer like that?

My First Time

The trading floor was a scrum of men screaming, signing and jockeying for position to execute their trades, an environment made all the more stressful by the inherent unpredictability of the markets. Newcomers were often overwhelmed.

CB: The starting bell would ring and the markets would open and there would be an eruption of noise. Just an absolute groundswell.

TC: I remember being on the observation deck and looking down on the Merc floor thinking There is no fucking way you’ll ever get me down there. Everyone’s running around like crazy, all these different colored coats. Then I ended up working there for 25 years.

MT: To an outsider, it must have looked like absolute chaos.

TC: It wasn’t long before I realized that in the chaos, there was order. It felt perfectly natural to be down there.

MT: It was scary shit. I was 22 years old, straight out of college, in a sea of men, and I had no idea what I was doing. It felt like being in world where you didn’t understand the language.

JL: The first day I was shaking. By the end of the week, I knew I could do it.

Hit the Floor Running

Getting a start on the trading floor meant first working as a runner, the lowest-level job there.

CB: You were literally a runner. There were no computers at the time, so the trades would come in off the phone, written down and the runner had to run them to the broker so he could fill the order.

DA: It paid $125 a week. Which wasn’t enough to live off, but it was an opportunity.

CB: It was a memorization job. You would get an order that said, “Buy five contracts for soybeans in November at X price.” So you had to know who was the buy broker for beans versus the sell broker, or the guy who bought for March. The training was getting yelled at. “Take this paper to this guy! Go there! Do it quick! Get back here!”

DA: People would scream at the top of their lungs right in the runners’ faces.

CB: You got yelled at because you couldn’t afford errors. If there was an error, you’d have to retroactively correct the contract, and by then the market has moved. Sometimes it worked in your favor; other times your firm had to eat it. They’d forgive you if an error occurred once every couple of months. If you screwed up once a week, they’d fire you.

DA: You started weeding them out then. About 30 percent made it to the next level.

Climbing the Ladder

After working as runners, people usually moved into support staff jobs such as phone clerk, fielding incoming orders from clients.

JL: I was a runner for two months, then I got an offer to be a clerk in the foreign currency exchange.

CB: When I worked in the summers, I didn’t care about the business. For me, it was just a summer job — 200 bucks a week for beer money and transportation. That was all I needed. But after I graduated college in 1982, I came back as a phone clerk, answering calls from customers and making sure their orders got to the brokers on the floor, and became fascinated with the business. It was exciting, it was real-time and it was a lot of responsibility. I was 24 and making $500 a week.

MT: I did a six month rotational program at O’Connor, gaining experience in each of the pits. It paid $16,500 a year. [$37,623.81 in today’s wages, according to the Bureau of Labor Statistics’ Consumer Price Index.] There wasn’t a lot of extra money, but they fed us breakfast and lunch and most of the bars served free food during happy hour.

CB: Show up on time every day, work hard, learn as much as you can — that’s all you had to do back then to move up. People would see you there everyday, and one day a guy would tap you on the shoulder and say, “I need a broker’s assistant. You interested?”

MT: I got a seat right on the floor right after the program, meaning I was allowed to execute trades there as opposed to working support staff. I was an idiot savant at options trading — give me three variables on a commodity and I could price it instantly.

TC: I learned early on the way to climb the ladder was to get large institutional customers and protect them. I spent two years in Australia and had a number of good contacts in London because of that, so I eventually became like a small business owner. I would go to whichever clearing house would cut me the best deal and bring my customers with me.

MT: After about a year and a half with O’Connor I was poached by a small trading firm named Schulco. They offered me 40 percent of the profits I made with no downside. I made $130,000 my first year with them and $250,000 my next year. I was 26 and I bought a house.

CB: I worked as assistant floor manager for about four years, helping manage the runners and phone clerks. So I made friends with the in-house counsel and became assistant compliance officer. I got to wine and dine customers whenever they were in town. This was the ’80s and commissions and interest rates were high. Money was being printed.

Life in the Pits

The most coveted, fast-paced and high-paying jobs were in the pits themselves, either as a broker, executing trades on clients’ behalves, or as a “local,” trading their firm’s and/or their own money.

CB: I’d always thought I wanted to be a floor broker, but I realized that I didn’t have the temperament for the pits. You had to be able to understand markets (which I didn’t) and be real quick at math (which I wasn’t). I had the temperament to run the desk, take orders, handle customers.

TC: Because we had to communicate across such a large distance, you had to be adept at signing. If your hands were facing your face, you were signalling you wanted to buy. Away from you meant selling. If you got that backwards …

JL: … you were in trouble.

DA: Signing was all eye contact. You had to lock eyes with someone to ensure your signals weren’t picked up by the wrong guy.

MT: You had to learn the sign language to the point it became second nature. After the first couple years we started using it in bars to signal how many beers we needed.

CB: There were “locals”; they traded their own money. They were the young guys who “got” the markets. And then there were order fillers, who traded on behalf of their firm’s customers and got paid a commission for every transaction. Some were making $1.75 per trade and filling 2,000 contracts a day. Others were making $4,000, $5,000 per day. So they didn’t care if the market went up, down or sideways — they wanted volatility. They were hardscrabble guys, fighting to get orders filled.

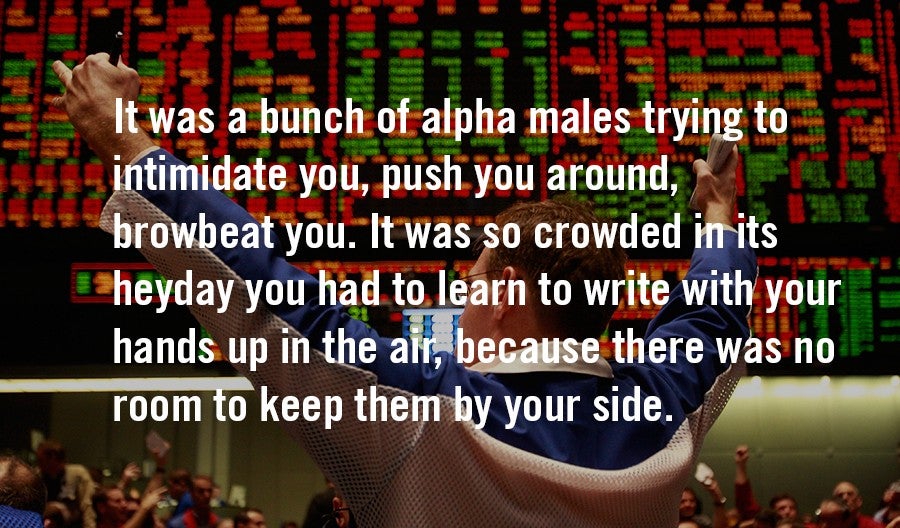

DA: It was a bunch of alpha males trying to intimidate you, push you around, browbeat you. It was so crowded in its heyday you had to learn to write with your hands up in the air, because there was no room to keep them by your side.

MT: You had to literally physically fight for your trades — screaming, fighting to stand in front of someone else. I probably weighed 120 pounds. I didn’t eat, didn’t sleep and drank like a fish. I’d leave the pit maybe three times a week, and that was to use the bathroom.

DA: Some people couldn’t handle the pressure. Their brains would lock, they’d lose their count and they were done.

MT: I had the advantage of having a higher pitched voice but I would get laryngitis from screaming all the time, so I ended up taking voice lessons to learn how to yell and breath from my diaphragm. After that, people could hear me a hundred yards away.

JL: We measured our pay by the month, not year. I made about $17,000 to $20,000 a month.

DA: I had months where I did $40,000 and months where I did $12,000.

MT: The most I ever traded in a day was probably 200,000 contracts (each with a value of $1 million), about 15 percent of the volume in the Eurodollars futures pit.

CB: Famous story: One day a guy walks into the soybean pit in the middle of the trading day carrying a hammer, a nail and a plant. He hammers the plant into the wall and people say, “What is that? What are you doing?” It was a soybean plant. These guys had been trading soybeans for years, some of them multi-millionaires, and they didn’t know what a soybean looked like. They didn’t have to.

TC: It required a skillset you couldn’t learn in a classroom: How to maintain confidence when the walls are burning down.

JL: You could never think about the money. I was doing billions of dollars worth of business a year, and that never crossed my mind. It can’t: you’ll panic.

MT: There was a psychological edge to being a female down there. I could just see when someone was nervous about filling a big order and I would take advantage. The men didn’t have that emotional quotient.

CB: Honestly, the guys who had business and economics degrees did worse. The guys who did better were the ones with art history and English degrees. Rules of economics don’t work in the futures market.

MT: The best traders were the ones who came from nothing because they were scrappers, they were hungry. The trust fund kids never made it.

DA: There were billions of dollars being exchanged, all on a handshake. You had to be a man of your word. If there was a discrepancy — say a guy says he sold me 300 contracts when it was actually 100 — and he wouldn’t make good on it, I’d say, “Either you’re gonna fix the fucking problem, or I’m gonna tell all my friends down here, and you will never get any trades through at any pit you go to.”

MT: In 1988, the FBI put moles on the floor of the Merc and CBOT, and they handed down some indictments for “trading on the curb,” which is legal now. But they couldn’t get any of the big traders because the big traders knew these moles weren’t on the up and up. There was something about them that set off everyone’s antenna. And if I didn’t know you, I wasn’t going to trade with you. It was 100 percent self-regulating that way.

DA: It was probably 65:35 men to women at the desk jobs. In the pits, probably 95:5.

MT: I would argue it was harder for women in other corporate environments than it was on the floor. Once you established yourself on the floor, people were gender blind, colorblind. If you were good at it, you were accepted.

JL: It really helped to have a sense of humor. Otherwise, that place could crush you.

MT: It was totally crude—talk about blowjobs, hookers, drugs. If you couldn’t stand that part of it, you didn’t even bother coming into the pits.

TC: There was a female filling broker in the Canadian futures pit who had a big order from Merrill Lynch, and she was looking to confirm a trade with a guy named Dick. But he was down in his cubicle so she couldn’t find him. She freaked out and screamed at the top of her lungs, “I NEED DICK NOW!” The place fell apart — everyone stopped for 30 seconds to laugh.

The Lifestyle

Although they say there is no accurate media portrayals of pit-trading life, the pit traders concede the partying often resembled The Wolf of Wall Street.

JL: We were making a lot of money for guys in their 20s, so we had fun. I spent it on cars, trips, booze, blondes.

CB: You had guys who were 25 driving $100,000 sports cars.

DA: Work would end and you’d race to get a good seat at the bar — Stocks and Blondes, Blackie’s, Alcock’s [no relation], Merc Club. Broker’s Inn — they’d fill your glass near to the top with booze, then put your mixer in. Three drinks there and you were done.

CB: Ceres Cafe [formerly Broker’s Inn], the bar-restaurant in the CBOT building, was a favorite of ours and famous for serving stiff drinks. Every drink order there is a double (whether you ask for it or not). It used to be in the Guinness Book of World Records for selling the most alcohol by volume of any place in the country.

TC: If you couldn’t handle the rigors of the partying, you wouldn’t maintain your job. Because the people were competitive about partying, too.

True story: One day Ricky Barnes — “Rocket Rick,” soybean trader — is at the bar when Terry Sheen tells him that he’s down $350,000. So Ricky switches to vodka, goes to the floor and not only does he get the 350 back, but makes another 200 on top of it. Then he had his own company a few years later called Barnes.

CB: Cocaine was huge. When I started as a phone clerk there were guys dealing coke under their desks and it took me half a year to realize it. They were making more money doing that than they were as a phone clerks.

MT: There were definitely some people coked out or drunk in the pit, but I never saw drugs myself.

JL: The hours were great. You’d go in about 6:45 in the morning, check your trades. Out of there by 2 p.m. most days and at Timber Trails golf course at 2:30. We called the unemployment numbers “unenjoyment” because we had to be on the floor when they were released on Fridays, but we wanted to take the day off. We’d come in for the first hour, get the numbers, then leave for the weekend.

CB: It was not uncommon for three brokers to leave early on Friday, hop in a cab to O’Hare, walk up to the ticket window and buy three first class tickets to Vegas (no luggage, paying cash). They’d party all Friday night, maybe get a room Saturday, Sunday take the red eye back to Chicago and show up to work on Monday in the same clothes they wore on Friday.

DA: A lot of people drank to unwind because the pit left them so stressed and wound up. Some nights I would drink all night, take a quick shower and come into work on no sleep. But you couldn’t do that every day.

MT: It was like playing in the world’s highest stakes poker game. Every day. You become into it for the risk alone. And to go home after that and try to be a real person and cook dinner … it was so hard to be two different people. It’s hard to talk mundane details with your girlfriends when you have $1 million at risk.

DA: The divorce rate was high. Guys would get out of the pits, go to the bar, meet a cute bartender and not go home. What did they care? They were making all the money in the world.

JL: It was hard to relate to people in other professions. They thought we were nuts.

MT: My husband and I bought all these houses — one in Miami, a ski house in Colorado, a big one in Chicago. All I was doing was working and he was fixing up these houses. And it was like, Are you fucking kidding me? I’m working so hard and you’re the only one enjoying it. One of the reasons my marriage broke up was I was working so hard to make this money, it took everything out of me.

TC: It’s a young man’s game. I wouldn’t want to put myself through that kind of pressure again.

The Gambling

Playing the markets is often referred to as legalized gambling. But when the markets were slow, the market-makers turned to gambling of the explicitly illegal kind.

CB: There was one guy who worked as a market reporter — they took the trades from the floor and entered them into the computer — and he would walk around all day handing out betting cards. You could bet college, pro — in broad fucking daylight in front of everybody.

MT: One day it was slow in the pit and the street outside was closed down. So some of the brokers made the eight fattest clerks race each other down the street and bet on it. There must have been 2,000 people lining the street watching.

DA: The Super Bowl pool was $1 million — 10K a square.

MT: There was hundreds of thousands of dollars changing hands each year during the NCAA tournament.

JL: The biggest bets were on the Masters. That was an exclusive group of the biggest guys on the floor and each bet was for thousands of dollars.

TC: A couple of crazies would take bets on whether they’d eat live cicadas.

CB: Some runners commuted in from Indiana. They made $250 a week as a runner and another grand buying cartons of cigarettes in Indiana, where they were cheaper, and selling them on the floor. On the 4th of July they did it with fireworks. They were just exploiting a spread, which is the same thing as trading.

https://www.instagram.com/p/BFhBuGuzFsU/

The Lows

Along with the chance to make hundreds of thousands (if not millions) of dollars was the risk you could lose just as much.

DA: I lost $40,000 one day, and I was laughing. My mentor goes, “What’s so fucking funny?” And I said, “That’s more than I made all last year. Don’t you think that’s kinda funny?” He said, “No, I don’t think that’s funny. That was my money.”

JL: I once had to write a check for $27,000 because of someone else’s error. But there were some people who got stubborn and lost millions and were never seen on the floor again.

MT: I’d come home some days after losing a ton of money and get in the fetal position for two hours. Because you feel like the biggest loser. There were definitely suicides and overdoses and alcoholism.

9/11

Although they worked in Chicago and not New York, the CBOT and CME workers were still in finance and thus professionally and personally affected by the September 11th terrorist attacks.

MT: It was like we were playing musical chairs. And then one day the music stopped.

DA: You could hear a pin drop.

MT: We were standing in the pit watching the big Jumbotrons in the corner. Standing behind me was a private pilot, and after the first plane hit he said, “That was too big to be a private plane.” We thought it might be a freak accident. Then the second one hit and we were all like Holy fuck, it’s an attack.

People thought we might get hit because we were close to the Sears [now Willis] Tower, and they left. But somebody had to stay and close the floor. It got eerily quiet, and they closed the markets early at 10:20 a.m.

TC: I was one of the last 20 guys there, working two different phones and six different markets until they closed the floor.

MT: I ended up walking home because I couldn’t find a cab. It was the most beautiful, gorgeous September day. We did a lot of business with Cantor Fitzgerald [the New York financial firm that occupied several floors in the World Trade Center] and the people we traded with were gone. I didn’t sleep well for six months. I thought Why am killing myself for this if it all be gone tomorrow?

CB: It took about six months for our business to bounce back.

MT: I stopped trading on the floor after that. It was just too much pressure. The markets dried up, and I had a huge, huge monster position, and it took me six months and cost me several million dollars to work my way out of it. But it was worth it to get out of there. I retired. I did nothing. I worked out every day and spent time with my daughter who was diabetic. About seven months later I was back on the floor.

Becoming Obsolete

The pits are now closed due to the financial industry being subsumed by investment banks and technology, a shift that began in the 1980s and accelerated in the early 1990s.

JL: Like with any industry, the biggest change was the introduction of the computer. What used to take a month took a week.

CB: In the late ’70s and early ’80s, people would say, “I bet they can computerize this.” And the heads of the pits would say, “We’ve brought in consultants to see if there’s a better way to do this than people screaming and waving hand signals at each other. They say, ‘There’s no better way. This is the most efficient way a market can run.’”

CB: Options were integrated into the market in 1980, and you had to be a lot smarter to trade options.

DA: The difference between futures and options is like the difference between checkers and three-dimensional chess.

JL: After the crash in 1987, the options market transitioned from being dominated by the locals to the investment banks. The bankers were assholes: They didn’t understand the culture and they brought in their own customers and cut prices.

DA: They were terrified of us. Then they cut us out.

TC: In 1992 they introduced Globex, [the first global electronic futures trading platform], as something that would work side-by-side with the traders. But the feeling was the machines were taking over.

DA: Globex cut out the middleman, the brokers and traders, and matched trades itself.

CB: About 90 percent of the trading in 1992 was done in the pit, and that slowly went down each year. Why? Because it might take you five minutes to call in an order and get it filled. With computers, it took five seconds. Nowadays, five seconds is an eternity. Orders are filled in five thousandths of a second.

MT: It really got bad in the mid-00s.The traders no longer had an edge — people would use our information and pick us off. I quit working on the floor in 2004 because I didn’t want to lose anymore money. It took a long time, but I realized I couldn’t beat the machines.

The Loss of a Culture

The Wild West culture of the pits has been replaced by a stodgy, corporate one.

CB: A lot of the guys from the floor couldn’t transition to the screen. A few them got back office jobs, but a lot were just put out of the business.

MT: On the floor you could just feel the market move. The noise, the emotion. That’s why it didn’t translate to an office job — you can’t take these agrarian traders and put them in a room by themselves. It’s sensory deprivation. Then you end up overtrading just to make it exciting, which ends with losing money. Their decades of trading just didn’t translate. They went into family businesses to make one tenth of what they used to.

CB: When we first started to get PCs, a guy was pretty much running a porn shop out of the IT room. He had more movies than you can imagine on his server. And nobody cared. But now if you tell a dirty joke in the office, you’re gone.

TC: I’m trying to think of any other business that would parallel the pits.

DA: Military. You were at war down there.

JL: It was kind of like being in a pit crew for auto-racing. The adrenaline.

CB: They took all the fun out of the business. I used to get excited to get up in the morning, call customers, have relationships. Not only did the markets get harder but the regulation got a lot tougher.

MT: We were insurers — we insured people’s risk and were paid a premium for it. The market appears to be less volatile now, but it isn’t. There’s no one to make markets and mitigate risk. You can tell by the “flash crash,” when the market dropped 1,000 points in 30 seconds on a random afternoon.

DA: The algorithm isn’t designed to take on risk, so the next meltdown is gonna be terrible. It’ll be 10 times worse than the housing and financial crises in 2008.

JL: The pits are deserted now. They put it on camera for CNN and the business channels, but nothing is going on.

MT: There’s absolutely nothing like it anywhere. It was just the coolest place to be and I felt so lucky that I had that experience, and I’m incredibly sad that my daughter will never get to see that.

John McDermott is a staff writer at MEL, where he recently interviewed the director of Game Face, a documentary about out LGBT athletes.